A Look At

Sponsor-Backed

Going Private Transactions

May 2013

Table of Contents

Introduction .................................................................................................................................... 1

Research Methodology ................................................................................................................. 2

United States ..................................................................................................................................3

Key Conclusions ..............................................................................................................4

New and Noteworthy ..................................................................................................... 5

Highlights of 2012 ..........................................................................................................8

Europe .......................................................................................................................................... 16

Key Conclusions ............................................................................................................ 17

Highlights of 2012 ........................................................................................................18

Asia-Pacific ...................................................................................................................................25

Key Conclusions ............................................................................................................26

Highlights of 2012 ........................................................................................................27

Representative Global Private Equity Partners .....................................................................30

About Weil .....................................................................................................................................31

1

Introduction

Welcome to our sixth survey of sponsor-backed going private transactions prepared by Weil, Gotshal & Manges

LLP. We hope that you will find this information thought-provoking and useful. We believe this survey is unique

in that it analyzes and summarizes for the reader the material transaction terms of going private transactions

involving a private equity sponsor in the United States, Europe, and Asia-Pacific. We believe Weil is uniquely

positioned to perform this survey given our international private equity platform and network of offices across

these regions. We are happy to discuss with clients and friends the detailed findings and analyses underlying

this survey. We want to offer special thanks to the many attorneys at Weil who contributed to this survey,

including Lewis Blakey, Patrick Brendon, Matthew Brush, Alexander Clavero, Jean-Baptiste Cornic, Allison

Donovan, Clementine Dowley, Joe Doyle, Lukasz Gasinski, Gabriel Gershowitz, Natasha Gopaul, James Harvey,

Darlyn Heckman, Mateusz Krauze, Peter Milligan, Harry Moseley, Renee Pristas, Bob Rivollier, Sandra Rutova,

Phillipp Schlawein, and Lei Yu.

Doug Warner

Founding Editor

Joshua Peck

Deputy Editor

Michael Weisser

Editor, United States

Andrew Arons

Deputy Editor

Samantha McGonigle

Editor, Europe

Matthew Speiser

Deputy Editor

Peter Feist

Editor, Asia-Pacific

2

Weil surveyed 40 sponsor-backed going private transactions announced from January 1, 2012 through

December 31, 2012 with a transaction value (i.e., enterprise value) of at least $100 million (excluding target

companies that were real estate investment trusts).

For United States transactions to be included in the survey, the transaction must have closed or such transaction

remains pending.

Twenty-four of the surveyed transactions in 2012 involved a target company in the United States, 10 involved a

target company in Europe, and 6 involved a target company in Asia-Pacific. The publicly available information for

certain surveyed transactions did not disclose all data points covered by our survey; therefore, the charts and

graphs in this survey may not reflect information from all surveyed transactions.

The 40 surveyed transactions included the following target companies:

Research Methodology

United States

Ancestry.com Inc.

Archipelago Learning, Inc.

Benihana Inc.

Deltek, Inc.

Duff & Phelps Corp.

eResearch Technology, Inc.

Great Wolf Resorts, Inc.

IntegraMed America, Inc.

Interline Brands, Inc.

ISTA Pharmaceuticals, Inc.

JDA Software Group, Inc.

Knology, Inc.

Mediware Information Systems, Inc.

MModal Inc.

P.F. Chang’s China Bistro, Inc.

Par Pharmaceutical Companies, Inc.

Sun Healthcare Group, Inc.

The Edelman Financial Group Inc.

The Talbots, Inc.

TNS, Inc.

TPC Group Inc.

Union Drilling, Inc.

Westway Group, Inc.

Young Innovations, Inc.

Europe

3W Power Holdings SA (Germany)

Arena Leisure plc (UK)

Douglas Holding AG (Germany)

EKO Holding SA (UK)

GlobeOp Financial Services SA (UK)

Goals Soccer Centres plc (UK)

Kewill plc (UK)

Marcolin SpA (Italy)

Mediq NV (Netherlands)

Misys plc (UK)

Asia

Adampak Limited (Singapore)

Adventa Berhad (Malaysia)

Discovery Metals Limited (Australia)

Luye Pharma Group Ltd. (Singapore)

Nexcon Technology Co., Ltd. (South Korea)

Spotless Group Limited (Australia)

3

United States

United States

4

The following is a list of key conclusions that we identified in our review of the 2012 US surveyed deals. The

Highlights of 2012 section contains additional analysis and information with respect to the 2012 surveyed deals.

▪

The number and size of sponsor-backed going private transactions were each lower in 2012 than in 2011 and

2010; however, when excluding the soft first quarter of 2012, deal activity was on par with such earlier years.

▪

Specific performance “lite” has become the predominant market remedy with respect to allocating financing

failure and closing risk in sponsor-backed going private transactions. Specific performance lite means that

the target is only entitled to specific performance to cause the sponsor to fund its equity commitment and

close the transaction in the event that all of the closing conditions are satisfied, the target is ready, willing,

and able to close the transaction, and the debt financing is available.

▪

Reverse termination fees appeared in all debt-financed going private transactions in 2012, with an average

single-tier reverse termination fee equal to 6.26% of the equity value of the transaction. Although outliers

remain, company termination fees are customarily in the range of 3-4% of the equity value of the transaction,

and reverse termination fees have trended consistently around 6-7% of the equity value of the transaction,

with reverse termination fees of roughly double the company termination fee becoming the norm.

▪

As was the case in 2011, no sponsor-backed going private transaction in 2012 contained a financing out (i.e.,

a provision that allows the buyer to get out of the deal without the payment of a fee or other recourse in the

event debt financing is unavailable).

▪

Some of the financial-crisis-driven provisions, such as the sponsors’ express contractual requirement to sue

their lenders upon a financing failure, have diminished in frequency. However, the majority of deals are silent

on this, and such agreements may require the acquiror to use its reasonable best efforts to enforce its rights

under the debt commitment letter, which could include suing a lender.

▪

Go-shops remain a common (albeit not predominant) feature in going private transactions, and are starting to

become more specifically tailored to particular deal circumstances.

▪

Tender offers continue to be used in a minority of going private transactions as a way for targets to shorten

the time period between signing and closing. There are two important developments with respect to tender

offers that impact sponsors, and these are discussed in the New and Noteworthy section of this survey.

▪

Increasingly, transaction agreements in 2012 included customized deal provisions tailored to the specific

facts and circumstances of each deal. As discussed in the New and Noteworthy section, this trend has

continued in 2013.

Key Conclusions

5

New and Noteworthy

The following is a list of new and noteworthy deal terms or concepts that have recently been seen in US

sponsor-backed transactions.

2013

In 2013, we have seen the return of mega-size deals that we have not seen since before the financial crisis,

with the proposed $23 billion acquisition of H.J. Heinz Company by Berkshire Hathaway Inc. and 3G Capital

and the proposed $24 billion acquisition of Dell Inc. by Silver Lake Partners, Microsoft Corp., and Michael Dell.

Separately, the Dell and Heinz deals are each larger in size than all of the 2012 sponsor-backed going private

transactions combined.

The Heinz and Dell deals both included partnerships between private equity sponsors and strategic investors

that were necessary to acquire such large public companies. The facts and circumstances of each of these

partnerships are very different, so it will be interesting to see whether the trend of these partnerships continues

in 2013 for larger deals and whether the debt markets can support additional deals of this size.

For example, many forces came together to get the Dell deal done. The large size of Michael Dell’s stake and

his willingness to roll over 100% in the deal (plus an additional investment from an affiliated investment fund),

the minimum $7.4 billion of cash accessible to the buying group, and the willingness of Microsoft to provide

approximately $2 billion of financing all came together to pave the way for this deal. Also of note, this transaction

was pulled off without structuring it as a traditional club deal.

In addition to these two megadeals, there were six other announced sponsor-backed going private transactions

in excess of $100 million through the first quarter of 2013, for a total of eight transactions. In 2012 there were

seven announced sponsor-backed going private transactions in excess of $100 million through the first quarter.

Although overall deal flow has not seen a major uptick in 2013, given the strong debt market it is not surprising

that many of the deals announced in 2013 are at values in excess of $1 billion. In addition to the Heinz and Dell

deals, the recently announced proposed $6.9 billion acquisition of BMC Software, Inc. by Bain Capital and Golden

Gate Capital is another example of a mega-size deal in the otherwise fairly subdued 2013 deal market.

Delayed reverse termination fee. While the recently announced Heinz deal generally follows the specific

performance lite construct, the reverse termination fee provision has a unique twist, which we think is

something that could catch on and be seen in future deals. In short, the reverse termination fee provision

seems to be designed to give the buyer some time to consider alternatives with respect to the financing

required for the transaction and, probably, to put pressure on the buyer to pursue a legal proceeding against

its lenders in the event such lenders fail to fund at closing if the conditions to funding have been met. In Heinz,

if a debt financing failure occurs, then Heinz may not terminate the merger agreement until: (i) if the buyer

does not initiate legal proceedings against its lenders to fund the required financing for the transaction or the

reverse termination fee, ten business days after notice of such failure to close; or (ii) if the buyer does initiate

such legal proceedings against its lenders, four months after notice of the failure to close or sooner if the

buyer has ceased to diligently pursue such legal proceedings against the banks. In addition, if during the four-

month extension period there is a material adverse effect (MAE), it will have no effect on the buyer’s obligation

to pay the reverse termination fee if otherwise required by the merger agreement. This remedy appears to

provide the buyer with added flexibility and time to address any holdup on the debt financing front.

6

New and Noteworthy

Limitation of matching rights during go-shop. Generally, after a target receives a superior proposal from

an alternative bidder, a buyer is provided with a period of three to five days to negotiate and match that

proposal. While rare, there have been outlier transactions that have included limitations on matching rights.

For example, in the 2010 take-private of Prospect Medical Holdings, Inc. by Leonard Green & Partners LP,

Leonard Green’s matching rights were eliminated if an alternative bidder offered a price that was 10% higher

than Leonard Green’s price. In the Duff & Phelps deal, we once again saw a limitation of matching rights: prior

to the go-shop “hard-stop” deadline, the buying group’s additional matching rights subsequent to initially

matching a go-shop bidder were eliminated. In addition, in the Dell deal, the buying group only has matching

rights on the initial competing bid (whether or not those rights are exercised during the go-shop period). With

respect to any pricing war that emerges or any subsequent competing offer, the matching rights completely

disappear. We will see if similar types of limitations on matching rights become more prevalent in 2013.

The VIP auction. In an effort to balance the confidentiality and competitiveness of a sale process (and to avoid

or minimize the often unfriendly market response to a failed auction), target boards have recently been utilizing

an approach that involves inviting a small group of select bidders to participate in an auction (rather than

undergoing a full auction). Given how expensive auction processes could be for sponsors, these “VIP” auctions,

where the sponsor may be one of a handful of bidders, could result in increased sponsor participation in such

processes. This type of selective auction process was utilized by Par Pharmaceuticals in its eventual sale to TPG

Capital, L.P. in late 2011.

Finding middle ground in the no-shop/go-shop dichotomy. Similar to the VIP auction discussed above, an

interesting provision was included in the Madison Dearborn–NFP transaction to achieve a balanced auction

process. In this case, a middle ground was established between the traditional no-shop restrictions and a formal

go-shop. While the agreement did not contain a go-shop provision, the agreement permitted other bidders that

were participating in the diligence process as of signing to continue to have access to the dataroom and diligence

materials for 30 days. Following this 30-day period, the “excluded party” concept customarily included in a go-

shop provision applied and NFP could continue the deal process with such excluded parties for an additional 15

days. The agreement applied a lower termination fee (75% of the normal termination fee) if the deal terminated

for a superior proposal with any party during the 30-day period (whether such party was an “excluded party” or

not) as well as if with an excluded party during the additional 15-day period. In the Benihana transaction, another

unique approach was used. The Benihana transaction agreement contained a go-shop, but if a superior proposal

was entered into during the go-shop period with a “Specified Party” (any of the 21 persons who entered into a

confidentiality agreement with the target in the eight months prior to signing in connection with any discussion

of a potential acquisition of the target), the target would have to pay the higher company termination fee (rather

than benefit from the reduced go-shop termination fee).

7

New and Noteworthy

Tender offer top-ups. One issue for sponsors with respect to tender offers is that these can be more difficult

to finance than the typical merger structure. This is due to the impact of the margin regulations limiting the

amount banks can lend against “margin” stock unless the shares tendered in the offer (together with any top-up

option) will be sufficient to complete a second-step, back-end merger immediately following the completion of

the tender offer. Therefore, a sponsor will need to ensure that the minimum condition is high enough for there

to be a sufficient number of target shares authorized to exercise the top-up option and increase the acquiror’s

ownership to 90% to be able to complete the back-end merger. This can lead to a situation where the percentage

of stockholders in favor of the transaction is very high (and definitely higher than the 50.1% generally required to

approve a merger), but the lack of authorized shares prevents the acquiror from exercising a top-up option and

closing the back-end merger immediately following the completion of the tender offer.

The Delaware bar has proposed an amendment to the Delaware General Corporation Law adding a new

Section 251(h). The amendment is intended to be effective as of August 1, 2013, and will address this issue

by eliminating the need for a top-up option if the parties expressly provide to proceed under the new Section

251(h). Under the proposed amendment, only 50.1% of the outstanding shares (or a greater percentage if

required in the charter) would be required to be tendered in the front-end tender offer for the back-end merger

to be completed without a stockholder vote. This both avoids uncertainty for an acquiror with a minimum

condition greater than 50.1% and eliminates the timing delay (and closing risk) of convening a stockholder

meeting and vote if the top-up option cannot be used.

Tender offer funding conditions. Another aspect of tender offers has been the regular inclusion of a

“financing proceeds condition,” or a funding condition, which is distinct from a financing condition. A funding

condition helps to ensure that a sponsor is not exposed to a failure of its financing sources to satisfy their

commitment, because as a technical matter the buyer must accept all tendered shares when all conditions

to the tender offer are satisfied. If there is a financing failure, the target’s remedy in a one-step merger with

specific performance lite is to seek the reverse termination fee, and the funding condition ensures that the

target’s remedy is the same in a two-step merger. It should be noted that, despite recent SEC comment

letters and responses to the contrary, based on “dual-track” sponsor-backed tender offers in the second half

of 2012, the SEC views funding conditions and financing conditions to tender offers in the same manner. As a

result, the SEC views the satisfaction of a funding condition or financing condition as constituting a material

change to the tender offer, requiring that at least five business days remain in the offer following disclosure

of this change. In all three tender offers with a funding condition in 2012, the sponsor ended up removing the

condition. This view by the SEC will require a strategic approach by private equity sponsors to ensure that they

have not committed to accepting shares tendered even though there has been a financing failure.

Majority of the unaffiliated. Going private transactions typically include a shareholder approval closing

condition. However, the recently announced Dell deal also includes a closing condition for the approval of a

majority of the unaffiliated stockholders of the company (i.e., excluding any shares owned by Michael Dell

or affiliates as well as any other officers, directors, buyer entities, or any of their affiliates). A majority of the

minority condition is more typically seen in deals where there is a majority controlling stockholder. Even with

Michael Dell rolling over his entire stake in the deal, the inclusion of a majority of the unaffiliated condition is

unusual as he only owns about 16% of the shares. This type of provision can be used in an effort to mitigate any

perceived conflicts of interest on a given deal. Time will tell if this type of provision becomes more commonplace

in private equity deals.

8

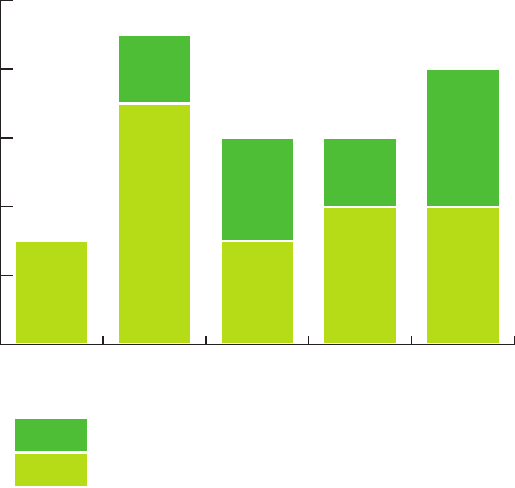

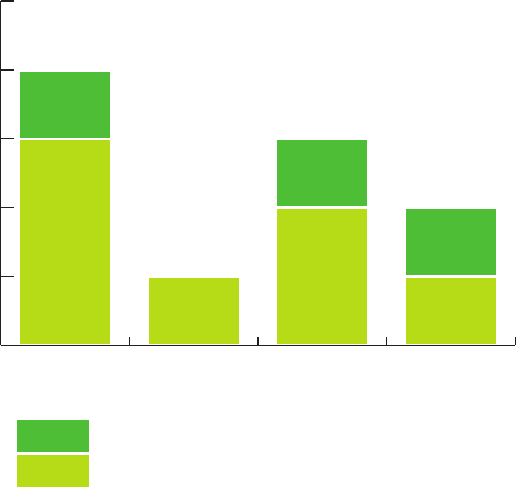

Sponsor-backed going private deal activity decreased in 2012, both in size of deals and deal frequency.

In 2012, there were 24 announced and currently pending or completed sponsor-backed going private

transactions in excess of $100 million, down from 33 and 35 such deals in 2011 and 2010, respectively.

However, this still represents a 71% increase over the depths of the financial crisis, when in 2009 only 14 such

transactions were entered into. Transaction values in our 2012 study ranged from $120 million to $2.1 billion.

The average deal size in 2012 was $714 million, compared with $1.25 billion and $1.49 billion in 2011 and

2010, respectively. The largest completed sponsor-backed going private transaction in 2012 was just under

$2.1 billion and the largest from 2010 and 2011 was just over $5.6 billion. The 24 surveyed deals had an

aggregate transaction value equal to approximately $17 billion, compared with aggregate transaction values

of approximately $41 billion in 2011 and $55 billion in 2010. Excluding the soft first quarter of 2012, sponsor-

backed deal activity was fairly consistent throughout 2012 (with between six and eight such deals per quarter)

and more on par with the two preceding years.

Highlights of 2012

0

2

4

6

8

10

2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1

More than $1 billion transaction value

$100 million to $1 billion transaction value

Going Private Market Activity in the US

(Excludes deals that were jumped, terminated,

or otherwise not consummated)

Number of

Transactions

Going Private Market Activity in the US

(Excludes deals that were jumped, terminated,

or otherwise not consummated)

Number of

Transactions

9

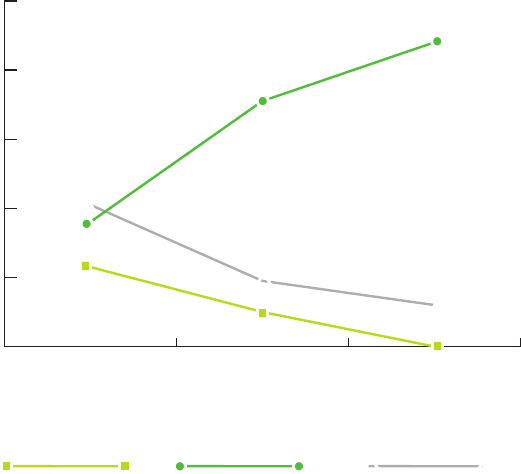

Specific performance lite is market. Specific performance lite, whereby the target has the limited right

to seek specific performance to force the closing only if all conditions to closing are satisfied and the debt

financing is available and ready to be funded, was utilized in approximately 88% of the 2012 surveyed deals

(compared with 74% in 2011 and 36% in 2010).

Highlights of 2012

Specific performance lite first emerged after the financial crisis as a compromise between targets, which

sought to limit the optionality built into the reverse termination fee structure, and sponsors, which could not

accept the risk of being forced to close transactions in the event their lenders failed to fund the debt proceeds

(in part due to “diversity” limitations in fund documents that restrict sponsors from investing more than a

specified percentage of the fund in any one deal). While specific performance lite was initially prevalent only

in larger buyouts (i.e., those in excess of $1 billion), it has clearly become the market remedy in middle market

buyouts as well. Outliers exist, but the specific performance lite model has become the accepted norm with

respect to allocating financing failure and closing risk in sponsor-backed transactions.

0%

20%

40%

60%

80%

100%

No Specific Performance

Specific Performance Lite

Full Specific Performance

2010 2011 2012

The Rising Use of Specific Performance Lite

Percentage

of Transactions

The Rising Use of Specific Performance Lite

Percentage of

Transactions

10

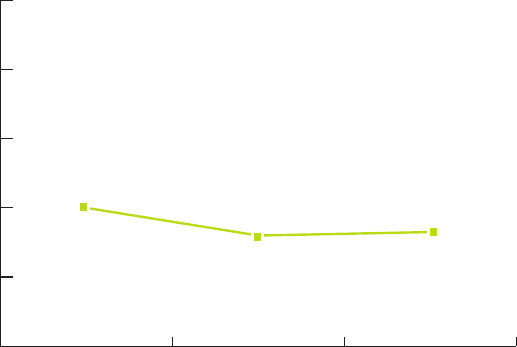

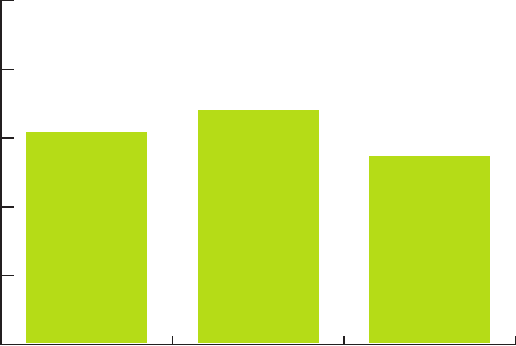

Use of go-shops was steady in 2012, but remains slightly down from 2010. While still a common feature

in many going private transactions, go-shop provisions that permit the target to canvas the market and solicit

other potential bids after a deal is announced have been somewhat less widely utilized in 2011 and 2012 (32%

and 33% of surveyed transactions, respectively) compared with 2010 (40% of surveyed transactions).

Highlights of 2012

Go-shops are often included as a way to assist a target’s board in maximizing shareholder value and are

particularly prevalent in transactions where the target’s board does not have the opportunity to commence a

full sales process or otherwise perform a market check prior to the signing of the transaction. The decrease

in the percentage of transactions in 2011 and 2012 that contain go-shops is likely indicative of the fact that

a larger number of deals in 2011 and 2012 were the result of competitive pre-signing processes, perhaps in

large part due to the seller-friendly environment resulting from the favorable debt financing market and the

large war chests of dry powder held by sponsors and strategics.

The length of the go-shop period in 2012 surveyed deals ranged narrowly from 30 days to 41 days, with an

average of 36 days. A hard-stop was utilized in all 2012 surveyed deals that contained a go-shop. A hard-stop

imposes a deadline (often an abbreviated period after the end of the go-shop period) on the target board to

negotiate a definitive agreement with a competing bidder solicited during the go-shop period in order for the

target to benefit from the reduced go-shop termination fee.

0%

20%

40%

60%

80%

100%

2010 2011 2012

Percentage

of Transactions

Use of Go-Shops in Going Private Transactions

Use of Go-Shops in Going Private Transactions

Percentage of

Transactions

Of the eight transactions with go-shops in 2012, six of the deals had hard-stops after the last day of the

go-shop period, which in such cases permitted the target to engage in negotiations with a competing bidder

solicited during the go-shop period for time periods typically ranging from 15 days to 30 days (with one outlier

of 2.5 days) after the end of the go-shop period. In two recently announced deals, the acquisition of Duff &

Phelps and the proposed acquisition of Dell (a 2013 transaction not included in our survey), we have seen the

hard-stop deadline and the period for the target to engage in negotiations with a competing bidder solicited

during the go-shop period trend toward the longer end of the range. In Duff & Phelps, after an initial 40-day

go-shop period, the target had an additional 28 days to negotiate and sign up an alternative deal and still

benefit from the reduced go-shop termination fee. The Dell deal went even further, providing Dell, after an

initial 45-day go-shop period, the right to negotiate and sign up an alternative deal with a competing bidder

solicited during the go-shop period up until the shareholders’ meeting and still benefit from the reduced go-

shop termination fee. Perhaps this extended period to negotiate and finalize a deal and still benefit from the

reduced go-shop termination fee has contributed to the submission of competing bids in the Dell deal prior to

the end of the go-shop period.

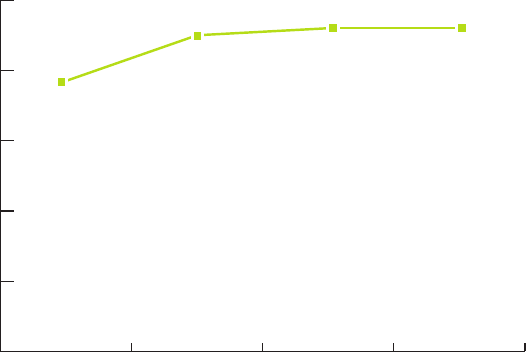

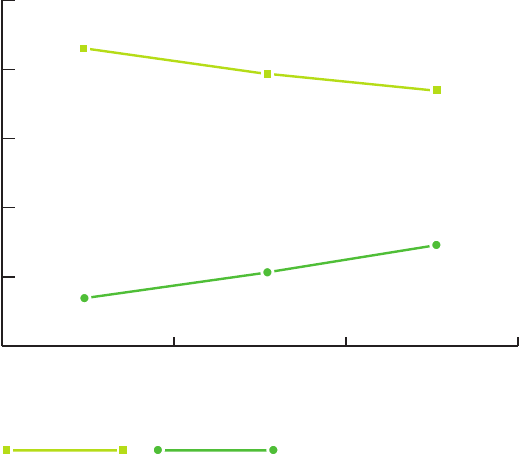

Termination fees payable in 2012 were consistent with prior years.

▪

Some form of reverse termination fee appeared in all of the surveyed transactions in 2012 other than two

transactions that were full specific performance “all-equity” deals. The average single-tier termination

fee in the 2012 surveyed deals that would have been payable by sponsors in certain termination scenarios

(e.g., financing failure) as a percentage of equity of the transaction was 6.26%, which is consistent with the

prior two years. The two-tier reverse termination fee construct, whereby the sponsor would pay a higher

reverse termination fee for willful breaches and/or refusal to close (other than in connection with a financing

failure), has been rarely utilized in recent years (it was only used in two surveyed deals in 2012).

11

Highlights of 2012

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012

Reverse Termination Fees Continue To Be Widely Used

Percentage of

Transactions

Reverse Termination Fees

Continue To Be Widely Used

Percentage of

Transactions

12

Highlights of 2012

▪

In the 2012 surveyed deals, the average termination fee as a percentage of equity value of the transaction

was 3.35%. This is the average termination fee that would have been payable by targets in certain

termination scenarios (e.g., entering into an alternative acquisition agreement in connection with a superior

proposal). It is consistent with, albeit down slightly from, the 3.49% average termination fee in the 2011

surveyed deals.

▪

In all of the 2012 surveyed deals with go-shop provisions, a superior proposal entered into as a result of the

go-shop triggered the payment of a reduced termination fee. Target boards took the view that the traditional

fee (~3.4%) was inconsistent with the spirit of the go-shop as a true post-signing “test the market” process.

On average, the reduced termination fee in the 2012 deals was 48% of the normal termination fee.

0%

2%

4%

6%

8%

10%

$100 million

to $500 million

Percentage of

Equity Value

$501 million

to $1 billion

Over $1 billion

Acquiror Termination Fee

by Equity Value

Acquiror Termination Fee by Equity Value

Percentage of

Equity Value

13

Highlights of 2012

In the 2012 surveyed deals, the typical tail period after the date of termination for which the entering into

or consummation of an alternative transaction would trigger a termination fee payable by the target was

12 months; however, 21% of the 2012 surveyed deals had nine-month tail periods. Further, 12.5% of the

2012 surveyed deals required that to trigger the termination fee, the alternative transaction be signed

and consummated within the tail period; 45.8% of the 2012 surveyed deals required that the alternative

transaction be signed within the tail period but the deal must ultimately be consummated at any time to

trigger the fee; and 41.7% of the 2012 surveyed deals required only that the alternative transaction be signed

within the tail period without a completion requirement.

Target termination fee scenarios. The five scenarios identified in the chart below are the most common

scenarios in which a termination fee must be paid by a target.

75%

80%

85%

90%

95%

100%

Target Company Terminates –

Superior Proposal/Fiduciary Out

Buyer Terminates – Target Company

Closing Condition Breach/Competing

Takeover Consummated During Tail Period

Either Party Terminates – No

Stockholder Approval/Competing

Takeover Consummated

During Tail Period

Buyer Terminates – Drop Dead

Date/Competing Takeover

Consummated During Tail Period

Buyer Terminates – Change

of Recommendation/Competing

Takeover Recommendation/

Notice of Superior Proposal

2010 2011 2012

Transactions with Termination Fees Paid

Upon Certain Scenarios

Percentage of

Transactions

Transactions with Termination Fees

Paid Upon Certain Scenarios

Percentage of

Transactions

14

Highlights of 2012

Ability of target board to change its recommendation. All of the 2012 surveyed deals contain provisions

allowing the target board to change its recommendation in certain situations to satisfy its fiduciary duties. Of

the 2012 surveyed deals:

▪

17% allow the target board to change its recommendation only in connection with a superior proposal.

▪

54% allow the target board to change its recommendation in connection with a superior proposal or an

“intervening event” (typically defined as an event or circumstance unknown or unforeseeable to the target

board at signing that now occurring or known would require the target board to change its recommendation

in order not to act in a manner inconsistent with its fiduciary duty).

▪

29% allow the target board to change its recommendation in connection with a superior proposal or if

required to satisfy its fiduciary duties generally.

Sponsors are not being required to sue their lenders. While initially popular following the financial crisis,

provisions expressly requiring sponsors to sue their lenders in the event that these lenders fail to provide

the committed debt financing have become less common. In fact, in 2012, only 21% of the surveyed deals

expressly contained such a provision (compared with a majority of the deals surveyed in 2010). It is important

to note, however, that the majority of deals are silent on this and such agreements may require the sponsor

to use its reasonable best efforts to enforce its rights under the debt commitment letter, which could include

suing a lender.

Tender offers continue to be popular, though they are still used in only a minority of going private

transactions. In 2012, sponsors utilized the two-step tender offer/back-end merger structure in 26% of the

surveyed deals (compared with 29% in 2011 and 15% in 2010). Tender offers have remained somewhat popular,

particularly due to the speed with which an acquisition structured through a tender offer (followed by a short-

form merger) can be completed (in as few as six weeks, if not less time) and now with the proposed amendment

to the Delaware General Corporation Law that would add a new Section 251(h) discussed in the New and

Noteworthy section, tender offers could become even more popular for sponsors.

Deals Structured as Tender Offers vs. Mergers

Percentage of

Transactions

0%

20%

40%

60%

80%

100%

Merger Tender Offer

2010 2011 2012

Deals Structured as

Tender Offers vs. Mergers

Percentage

of Transactions

15

Highlights of 2012

Dual-track tender offers. Of the surveyed deals that utilized the two-step tender-offer/back-end merger, 57%

of such deals used the dual-track approach. Under the dual-track approach, the process for a tender offer

(beginning with the filing of a Schedule 14D-9 and Schedule TO) and one-step merger (beginning with the filing of a

preliminary proxy statement for SEC review) are initiated at roughly the same time. As such, if the tender offer fails,

the target will have avoided significant timing delays by having already commenced the proxy statement process

in a one-step merger. SEC staff members have questioned whether the filing and/or mailing of a proxy statement

prior to the expiration or termination of a contemporaneous tender offer was consistent with Rule 14e-5 of the

Exchange Act (which prohibits a buyer from purchasing target securities outside of a tender offer). However, a dual-

track approach may no longer be necessary to create a timing advantage due to the proposed amendment to the

Delaware General Corporation Law of adding a new Section 251(h) discussed in the New and Noteworthy section.

16

Europe

17

Key trends for going private transactions in Europe in 2012 include:

▪

After a slow 2011, 2012 saw the UK return to its prior status as the most popular market for sponsor-backed

going privates in Europe, with 50% by volume and 45% by value of announced deals in 2012 involving UK-listed

targets.

▪

Schemes of arrangement remain the going private structure of choice for UK-incorporated targets due to

the ability to acquire 100% of the target with only 75% shareholder approval in a shorter period of time (offer

requires 90% acceptance and for the bidder to subsequently follow the statutory squeeze-out regime) and to

avoid stamp duty (i.e., transfer taxes payable on an offer).

▪

In blocking Nordic Capital’s offer for 3W Power Holdings, the Bundesanstalt für Finanzdienstleistungsaufsicht

(Germany’s takeovers regulator) confirmed that it is unwilling to approve an offer that is subject to a “No MAC”

condition unless it is drafted such that only events that occur following the date of the offer are capable of

triggering the condition.

▪

The September 2011 amendments to the UK Takeover Code have not proved to be as problematic for sponsor-

backed going privates as was originally feared (in fact, both the value and volume of sponsor-backed going

privates increased in 2012), although some concerns do remain around the requirements for:

▪

targets to publicly identify bidders at certain times under certain circumstances; and

▪

bidders to disclose full details of their financing arrangements, especially market flex provisions, at the

time of announcement.

▪

Following on from the September 2011 amendments to the UK Takeover Code, there is evidence in other

European jurisdictions (for example, the Netherlands) of a trend toward restrictions on how the bidder operates

a target post-closing. Perhaps most strikingly for sponsors, it is becoming customary in the Netherlands for a

“responsible financing” covenant to be given (for example, that the target will not be leveraged above a certain

multiple).

▪

2012 saw a number of competitive going private processes where sponsors competed both against each other

and against strategics for listed European targets.

Key Conclusions

18

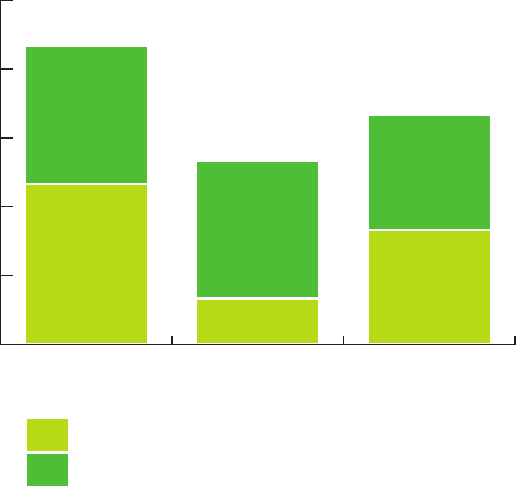

Sponsor-backed going private deal activity increased in 2012 against 2011, but remains down from 2010.

In 2012 there were 10 announced sponsor-backed going private transactions in excess of $100 million in Europe

with a total value of $7.8 billion, a 25% increase from 2011 by volume (2011: 8 deals) and a 56% increase by

total value (2011: $5 billion). However, activity is still down from 2010; 13 deals were announced in 2010 with

an aggregate value of $11.5 billion, while 3 of the only 10 deals announced in 2012 were aborted because of

insufficient shareholder support (Goals Soccer Centres), a higher subsequent offer (GlobeOp Financial Services),

or regulator intervention (3W Power). The average announced deal size in 2012 was $780 million, again higher

than the 2011 average of $620 million, but still down from the 2010 average of $884 million. The 2012 deals

surveyed ranged in size from $109 million to $2.3 billion, which is also similar to the 2011 range of $136 million

to $2 billion.

Highlights of 2012

Activity is Rebounding in Numbers of Deals . . .

Number of

Transactions

0

3

6

9

12

15

2010 2011 2012

Number of

Transactions

Activity is Rebounding in Numbers of Deals . . .

. . . and in Total Value

Total Transaction

Value (Billions)

0

3

6

9

12

15

2010 2011 2012

$11.5 Billion

$5.0 Billion

$7.8 Billion

Total Transaction

Value (Billions)

. . . and in Total Value

19

Highlights of 2012

Generally consistent deal flow. Excluding the slow second quarter (with only one transaction valued at just

$136 million), deal activity was fairly consistent during 2012, with two to four transactions per quarter, one

of which was $1 billion or more. The first quarter of 2012 was the standout, with both the most deals (four)

and the highest aggregate value ($3.6 billion). However, in the first quarter of 2013, only one sponsor-backed

going private transaction in excess of $100 million has been announced in Europe, the proposed $1.74 billion

acquisition by Foundation Asset Management and Lindengruppen of Höganäs. This slowing of deal flow is

reflective of a slow first quarter for European private equity buyouts generally; a recent Preqin survey shows

that, by aggregate deal value, in the first quarter of 2013 private equity buyouts had their worst quarter since the

third quarter of 2009. Nevertheless, the Foundation Asset Management–Lindengruppen transaction does exhibit

(albeit on a smaller scale) the sponsor/strategic collaborations seen in the recent Heinz and Dell transactions in

the US.

Going Private Market Activity in Europe

Number of

Transactions

0

1

2

3

4

5

2012 Q1 2012 Q2 2012 Q3 2012 Q4

Over $1 billion

$1 million - $1 billion

Number of

Transactions

Going Private Market Activity in Europe

20

Return of the UK. 2012 saw the return of the UK as the most popular market for sponsor-backed going privates

in Europe as it was in both 2010 and 2009, with 50% by volume and 45% by value of announced deals in 2012

involving UK-listed targets.

Highlights of 2012

Competition for public targets. As in the US, sponsors competed against each other (and against strategics)

for public targets across Europe (including in the UK, despite the new rules discussed below which many feared

would significantly impair UK going privates). For example:

▪

UK targets:

▪

Vista Equity Partners acquired Misys for $2.3 billion following a highly competitive (and public) auction

involving sponsors CVC Capital Partners and ValueAct Capital, as well as strategic Temenos Group.

▪

TPG made a $716 million offer for GlobeOp, which was subject to competition from Advent International

(although strategic SS&C prevailed after trumping TPG with a higher offer).

▪

Francisco Partners and Symphony Technology Group both made offers for Kewill before Francisco’s

enhanced $125 million offer was successful.

▪

Polish target:

▪

Advent International and Mid Europa Partners both made several offers during a month-long bidding war

for EKO, before Advent International (having sweetened its offer three times) finally secured a 98% stake

at the end of October 2012.

▪

Italian target:

▪

BC Partners acquired a majority stake (as a precursor to a mandatory offer to minority shareholders) in

Gruppo Coin following a competitive auction involving many of the leading European and global sponsors,

including Apax Partners, Bain Capital, Carlyle, and CVC Capital Partners.

Transaction Jurisdiction

Volume

0

3

6

9

12

15

2010

Other

United Kingdom

2011 2012

Transaction Jurisdiction

Volume

21

Structuring preferences. For UK-incorporated targets, schemes of arrangement continue to be the acquisition

structure of choice (2012: all deals, 2011: all deals, 2010: six out of seven deals) due to the ability to acquire

100% of the target with only 75% shareholder approval and in a shorter period of time (offer requires 90%

acceptance and the bidder to subsequently follow the statutory squeeze-out regime) and to avoid stamp duty

(i.e., transfer taxes payable on an offer).

Unusually, a majority of listed Italian companies are held by controlling shareholders. Therefore, sponsor-

backed going privates of Italian targets are almost always structured as privately negotiated acquisitions of the

majority stakes held by such controlling shareholders followed by mandatory offers for the remaining shares

and, ultimately, a squeeze-out of minority shareholders (once the bidder owns 95% of the target). Both of the

sponsor-backed going privates of Italian companies in the last two years (PAI Partners’ acquisition of Marcolin

and BC Partners’ acquisition of Gruppo Coin) used this structure.

Restrictions on the target’s business post-closing. We have seen evidence of a general trend in Europe toward

bidders being bound to operate the target’s business in a particular manner post-closing. The UK Takeover

Code was amended in September 2011 to make certain statements that the bidder is required to include in

the offer document (for example, the bidder’s intentions regarding the post-closing strategy of the target and

the impact of that strategy on the target’s employees and places of business) binding on the bidder for 12

months post-closing absent a material change of circumstances. This amendment was made in response to

Kraft’s controversial closure of a Cadbury factory after Kraft had confirmed that it did not intend to do so in

its offer document. Perhaps unsurprisingly given that targets are not integrated into a larger operating group

on a sponsor-backed going private (unless it is a bolt-on acquisition), sponsors have tended to deal with this

requirement with a simple statement that they intend to continue business as usual post-closing.

Further, in the Netherlands, there has been an interesting trend toward increased post-closing commitments

that are enforceable against the bidder by the former independent directors of the target. Previously, bidders

were asked to make public statements regarding their intentions which were not directly enforceable. This

trend toward increased commitment is driven by two factors: (i) the fiduciary duties of directors of Dutch targets

require them to take into account the interests of a broader group of stakeholders (including employees and the

communities in which the target is based) in addition to shareholders when deciding whether to recommend

an offer for acceptance; and (ii) directors seeking to avoid being subject to the kind of adverse public reaction

that has been seen against former directors of other companies which were subject to post-closing overhaul.

While, as in the UK, many of the commitments sought by boards are more controversial for strategic bidders

(for example a commitment to continue the business as is, including branding, not to close sites, and not to

make large-scale redundancies for a period of time post-closing), there are two emerging requests that may be

controversial to sponsors:

▪

to maintain “proper financing” post-closing (on its offer for Mediq, Advent International agreed that Mediq

would not incur additional indebtedness if it would result in Mediq’s debt-to-EBITDA ratio exceeding 4.0); and

▪

to keep a minimum number of independent directors on the board of the target for a period of time post-

closing (on its offer for Mediq, Advent International agreed that Mediq must have at least one independent

director until the earlier of: (i) four years post-closing; and (ii) an exit).

Highlights of 2012

22

Conditionality. In blocking Nordic Capital’s offer for 3W Power, the Bundesanstalt für Finanzdienstleistungsaufsicht

confirmed that it is unwilling to approve an offer that is subject to a “No MAC” condition unless it is drafted such

that only events that occur following the date of the offer are capable of triggering the condition.

However, Germany’s takeovers regulator is willing to approve an objective condition based on general market

performance, such as that in Advent International’s offer for Douglas Holding that the MDAX close at 8,800

points or above on the last day of the offer period. In the UK, although the bidder could make an offer subject

to such a condition because it is objective (a common implementation of the requirement in the EU Takeovers

Directive that each Member State enact rules governing permissible conditions), the UK Takeover Code goes

one step further. It prohibits (subject to limited exceptions for conditions relating to acceptance level or UK or

EC antitrust review) bidders from invoking any condition unless the circumstances giving rise to invocation are

of material significance to the bidder in the context of the offer. The Takeover Panel has adopted a very strict

interpretation of this standard when matters other than mandatory antitrust or regulatory clearances are at

issue, and because the MDAX condition relates to general market conditions, it is doubtful that a bidder could

rely on such a condition in the UK.

Impact of UK reform. The September 2011 changes to the Takeover Code were seen, at the time of reform,

as a significant potential impediment to sponsor-backed going privates, but this fear has not been borne out

in practice (both deal volume and deal value increased from 2011 to 2012). Broadly, the changes that caused

concern, and the reasons why those concerns have not materialized as feared, were as follows:

▪

Introduction of a requirement for the target to publicly name which bidders it is in discussions with

when the target is subject to rumor/speculation or unusual share-price fluctuations. A publicly named

bidder then has 28 days to make an offer or it will be prohibited from doing so for six months (“put up or

shut up”).

▪

These requirements caused concern both because sponsors generally are averse to being publicly

confirmed as interested in an acquisition before signing and because it was feared that the automatic

“put up or shut up” deadline would be used by targets to pressure bidders to complete their diligence and

present fully financed bids in a short period of time or else be unable to make an offer for six months.

Extensions to the 28-day deadline are only available with the consent of the Takeover Panel, which will

generally only give them at the request of the target’s board. However, both concerns have become an

accepted part of going private processes in the UK due to the reality that target boards generally have

agreed to extend the 28-day deadline where constructive discussions are ongoing. (Not to do so may be

in breach of their fiduciary duties.) Although most of the sponsor-backed going privates in 2012 were

announced within the initial 28-day period, Ontario Teachers’ Pension Plan Board’s period to make an offer

for Goals Soccer Centres was extended several times and ended up being in excess of 100 days in total.

In addition, these requirements have created an unequal playing field for bidders entering the process

at different times. The new requirements allow late entrants to fly under the radar and confidentially

investigate the target while the interests of others (who are also subject to the “put up or shut up”

deadline) are public. One example of this was SS&C’s trumping TPG’s offer for GlobeOp. GlobeOp had

been subject to rumor/speculation and was therefore required to announce that it was in discussions with

TPG and Advent International (the two potential bidders) at the time. Subsequently, SS&C approached

GlobeOp, but public identification of SS&C’s intent was not required because GlobeOp was not subject to

further rumor/speculation or unusual share-price fluctuations. As a result, the first that the market heard

of SS&C’s interest was after TPG had completed its diligence and announced a fully financed offer (at a

no doubt substantial cost to TPG), when SS&C announced that it was considering its position and urged

shareholders not to accept TPG’s offer until SS&C made a further announcement.

Highlights of 2012

23

▪

Expansion of prohibitions on deal protections to generally prohibit the target from agreeing to anything

with a bidder or its concert parties in connection with an offer.

▪

Pre-September 2011, certain limited deal protection was permissible in the UK. For example, it was

customary to have an implementation agreement between the bidder and target by which the parties

agreed to the offer process (especially if the offer was to be implemented by way of a scheme of

arrangement, a court process initiated by, and under the control of, the target) and which may have

contained provisions such as a termination fee payable by the target (capped at 1% of the target’s value

calculated by reference to the offer price) under certain circumstances. Now, subject only to very limited

exceptions, all such agreements (including “no-shop” and “no change of recommendation” provisions,

which are permissible in other jurisdictions, including the US) are prohibited. At the opposite end of

the spectrum, and subject to an exception permitting searches for higher offers so as to maximize

shareholder value, target boards have long been prevented from taking defensive measures against offers

without shareholder consent (on the basis that whether or not to accept an offer should be a decision

for shareholders without director intervention). The prohibition on directors agreeing to deal protection

is arguably a logical extension of that principle to subsequent offers, the deliverability of which can be

significantly impaired by deal protection agreed with an earlier bidder.

The fear, however, was that the lack of deal protection would dissuade bidders from pursuing going private

transactions because of reduced deal certainty, even for an offer that had the full support of the target

board at the date of announcement. In particular, a target can unilaterally cancel a scheme of arrangement

if the board changes its recommendation. However, given the increase in both sponsor-backed deal volume

and value in 2012 as against 2011, clearly this has not materialized. Instead, bidders have:

▪

Sought stronger shareholder commitments

1

from a larger number of institutional shareholders.

Excluding director/manager irrevocables (which are almost always given in “hard” format where a

recommendation/roll-over commitment is received), of the six 2012 UK transactions surveyed, the three

that failed to complete (which include the competing offer for Kewill by Symphony Technology, which

was defeated by Francisco Partners’ offer) all had far lower levels of shareholder commitments at the

date of announcement than those that went on to complete:

▪▪

Aborted transactions:

▪▪

TPG’s offer for GlobeOp Financial Services: 5% of shares subject to “soft” irrevocable undertakings

and 7% subject to letters of intent.

▪▪

Ontario Teachers’ Pension Plan Board’s offer for Goals Soccer Centres: 13% of shares subject to

letters of intent.

▪▪

Symphony Technology’s offer for Kewill: 9% of shares subject to “semi-hard” irrevocables with a

10% hurdle.

Highlights of 2012

1 Shareholder commitments are customarily given in one of four formats:

a. “Hard” irrevocable undertakings: unconditional undertakings to accept the offer.

b. “Semi-hard” irrevocable undertakings: undertakings to accept the offer unless an offer that is higher by a threshold amount is

announced.

c. “Soft” irrevocable undertakings: undertakings to accept the offer unless any higher offer is announced.

d. Letters of intent: non-binding statements of intention to accept the offer.

24

Highlights of 2012

▪▪

Completed transactions:

▪▪

Vista Equity’s offer for Misys: 22% of shares subject to “semi-hard” irrevocables with a 10% hurdle.

▪▪

Aldersgate Investments’ offer for Arena Leisure: 71% of shares subject to “semi-hard” irrevocables

with a 13% hurdle and undertaking to remain binding so long as the bidder at least matched any

higher offer.

▪▪

Francisco Partners’ offer for Kewill: unusually, 25% of shares subject to undertakings not to accept

any competing offer unless announced within ten days and at least 7.5% better (note: Francisco

Partners’ offer was not 10% higher than Symphony Technology’s, so those who signed the

irrevocable undertakings in favor of Symphony Technology were still bound).

▪

In unusual situations, sought deal protection akin to terminations from key stakeholders in the target.

This has only happened twice to date, and neither situation involved a sponsor.

▪

Expansion of the rules concerning descriptions of financing to require full disclosure of a bidder’s

financing terms on announcement, including any market flex provisions.

▪

The fear was that sponsors, which are often reliant on bank financing, would be disadvantaged because

financing agreements are typically signed on announcement and the requirement immediately to disclose

market flex provisions would allow no time to syndicate the debt in the usual confidential manner.

Therefore, syndicatees would be likely to ask for pricing at the top of the flex. Typically, market flex

provisions are “active” for a maximum of six months post-completion, subject to early termination if

syndication is successfully completed within that time.

The UK Takeover Panel has tended to offer a partial concession to this rule since its introduction and

allows market flex provisions to be disclosed upon posting of the offer/scheme document, which results

in a period of up to 28 days post-announcement during which syndication can take place on customary

confidential terms. Both Vista Equity (on its offer for Misys) and TPG (on its offer for GlobeOp) obtained

such a concession, although in neither case did the bidder take advantage of the full 28-day period (Vista

posted ten days post-announcement and TPG 14 days post-announcement). Further, the extent to which

this period of confidential syndication offers any legal protection is unclear because, although a sponsor

may be comfortable on a commercial level that any debt can be successfully syndicated pre-posting,

market flex provisions customarily remain “active” until a maximum of six months post-closing (i.e., long

after they are required to be made public).

25

Asia-Pacific

26

Key Conclusions

In 2012, total private equity activity in Asia-Pacific

1

decreased more than 40% from 2011 and approximately 10%

from 2010. There was also a decrease in the number and transaction value of surveyed sponsor-backed going

private transactions in the region. Six going private transactions form part of our survey this year, and constitute

about 5% of private equity activity, by deal value, in the region.

Some conclusions and trends for going private transactions in the region for 2012 include:

▪

The 6 sponsor-backed going private transactions surveyed in 2012 represented a significant decrease from 14

transactions in 2011 and 8 transactions in 2010.

▪

As in prior years, schemes of arrangement and tender offers continued to be the two principal forms used in

takeover bids.

▪

Sponsors in the region often finance their acquisition with equity only, and transactions with debt financing are

in the minority. In 2012, only one of the six surveyed transactions had debt financing.

▪

Termination fee provisions are often seen in transactions effected through a scheme of arrangement, some of

which also contain reverse termination fee provisions. If used, reverse termination fees in the region tend to be

similar in size to termination fees.

▪

Fiduciary outs are treated very differently in different jurisdictions in the region. In some jurisdictions, a

fiduciary out provision is common in a scheme of arrangement. In other jurisdictions, a fiduciary out provision is

prohibited without shareholder approval.

▪

Go-shop provisions remain a relatively unused concept in the region. None of the surveyed transactions in

2012, 2011, or 2010 had a go-shop provision.

▪

Financing-out provisions are uncommon in transactions in the region. For transactions effected by cash offer,

typically certainty of funding has to be confirmed before the offer can be launched. For transactions effected

by a scheme of arrangement, a financing condition can sometimes be included in the scheme agreement, but

often all conditions must be satisfied before the scheme can be sanctioned by a court.

▪

An MAE-out is common in many jurisdictions in this region, except it is typically not permitted in mandatory

offers. In some jurisdictions, an MAE-out has to be objective, while in other jurisdictions it is possible to have a

broader, more subjective MAE.

▪

As with previous years, a number of sponsor-backed going private “indicative proposals” in the region were

either rejected by the target or withdrawn, or otherwise did not result in a definitive agreement. As a result,

these “indicative proposals” are not reflected in the survey.

1 For the purposes of this survey, the Asia-Pacific region includes Australia, China (including Hong Kong), India, Indonesia, Japan, South

Korea, Malaysia, New Zealand, Philippines, Singapore, Taiwan, Thailand, and Vietnam. Information regarding market activity is based on

publicly available information and has not been independently verified.

27

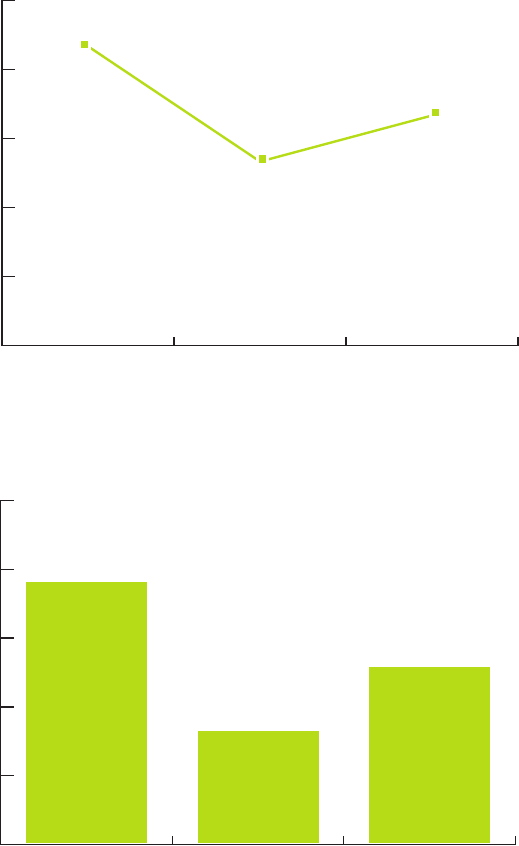

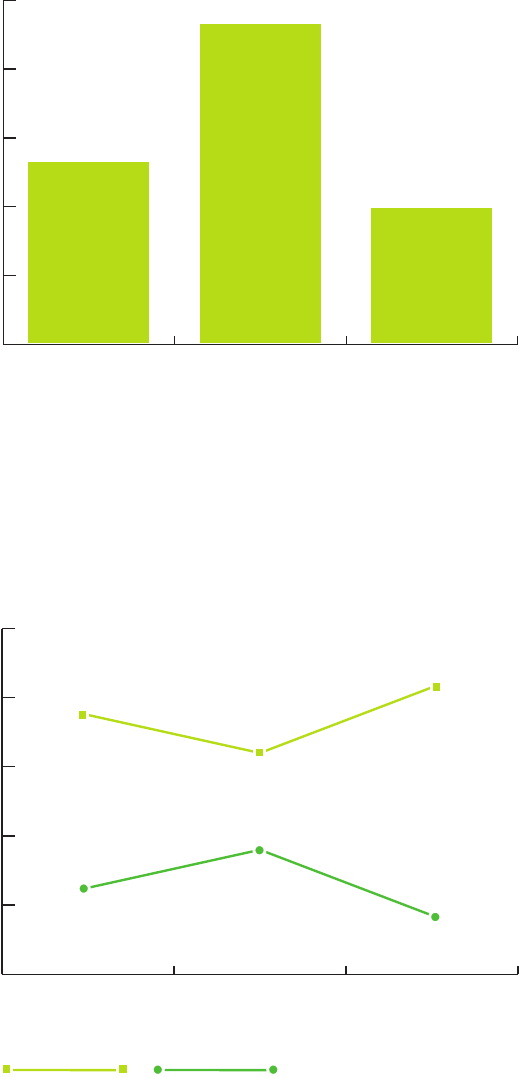

Sponsor-backed going private deal activity decreased in 2012. In 2012, there were 6 announced sponsor-

backed going private transactions in excess of $100 million in the region included in our survey, down from 14

and 8 such deals in 2011 and 2010, respectively. Transaction values of the six surveyed 2012 deals ranged from

just over $100 million to just over $1 billion. The six surveyed deals represent an aggregate transaction value

equal to approximately $2.8 billion, compared with aggregate transaction values of approximately $9.2 billion in

2011 and $7.1 billion in 2010.

Tender offers and schemes of arrangement are the more commonly seen takeover forms in the region.

As would be expected, the legal regimes applicable to public takeovers in the jurisdiction of the target

company determine the form of the transaction. As in previous years, the transactions surveyed in 2012 were

accomplished by either a cash offer for shares or a scheme of arrangement. Cash offers continue to be the more

popular form for the surveyed transactions in this region.

Highlights of 2012

Going Private Market Activity in Asia-Pacific

Number of

Transactions

0

3

6

9

12

15

2010 2011 2012

Number of

Transactions

Going Private Market Activity in Asia-Pacific

Transactions Structured as

Tender Offers vs. Schemes

Percentage of

Transactions

0%

20%

40%

60%

80%

100%

Tender Offer Scheme

2010 2011 2012

Transactions Structured

as Tender Offers vs. Schemes

Percentage

of Transactions

28

Transactions with debt financing continue to be in the minority. In 2012, only one out of the six surveyed

transactions (or approximately 17%) had debt financing, down from 43% in 2011 and 50% in 2010. As can be

expected, debt financing appears to be more commonly used by sponsors in more mature markets in the region.

Termination fees continue to appear in transactions effected through a scheme. Consistent with the findings

in previous years, the single surveyed transaction effected through a scheme of arrangement in 2012 included a

termination fee payable by the target if the transaction was terminated as a result of a superior offer or certain

material breaches by the target. This surveyed transaction also contained a reverse termination fee clause which

was otherwise similar to a reverse termination clause in US deals, except the size of the reverse termination fee

was the same as the termination fee. Reverse termination fee clauses are generally less common in Asia-Pacific

markets than in the United States. In some jurisdictions in this region, termination fees are normally at or below

1% of the transaction value.

Highlights of 2012

Transactions with Debt Financing

Percentage of

Transactions

0%

20%

40%

60%

80%

100%

2010 2011 2012

Transactions with Debt Financing

Percentage of

Transactions

Scheme Deals with Termination Fee

or Reverse Termination Fee

Percentage of

Transactions

0%

20%

40%

60%

80%

100%

Termination Fee Reverse Termination Fee

2010 2011 2012

Scheme Deals with Termination Fee

or Reverse Termination Fee

Percentage of

Transactions

29

Different jurisdictions in this region have a very different take on the fiduciary out provision (or ability of the

target board to change its recommendation). There are great variations among jurisdictions in this region with

respect to fiduciary out. In a few jurisdictions, such as Australia, the target board usually negotiates a fiduciary

out in a scheme of arrangement, while the buyer usually negotiates a notification right, a matching right, and a

termination fee if the target accepts a competing bid. At the other end of the spectrum are jurisdictions where a

fiduciary out provision is generally not legally permitted without obtaining shareholder approval.

Go-shop provisions remain a relatively unused concept in the region. Go-shop provisions have been rare in all

jurisdictions in the region, even in more mature markets such as Australia. None of the surveyed deals in 2012,

2011, or 2010 had go-shop provisions. In transactions effected through a scheme of arrangement (which typically

involves direct agreements with the target company), targets usually agree to a no-shop or similar provision.

Financing-out provisions are unusual in going private transactions in this region. In most jurisdictions in the

region, if the transaction proceeds by way of a cash offer, then at the time the offer is launched the buyer must

have certainty of funding (sometimes the buyer must obtain an unconditional confirmation from its financial

adviser or a bank). If the transaction proceeds by way of a scheme, then a financing condition can sometimes be

included in the scheme agreement (and the buyer may be required to pay a reverse termination fee if it cannot

successfully obtain financing), but all conditions must be satisfied before the scheme can be sanctioned by

a court. In some jurisdictions, it is possible to structure the transaction as a pre-conditional offer, so that the

offer is formally launched only after the financing condition is met. Sometimes such pre-launch “financing out”

requires pre-clearance from the relevant regulatory authority.

MAE-out provisions are common in transactions in this region. It is common to have an MAE-out in

transactions in many jurisdictions in this region, except an MAE-out is typically not permitted in mandatory offers

(which normally can be subject to only one condition, the voting threshold). In some jurisdictions, an MAE-out

has to be sufficiently objective and its fulfilment cannot depend on the subjective interpretation or judgment by

a transacting party, while in other jurisdictions, it is possible to have a broader, more subjective MAE. Sometimes

an MAE-out requires pre-clearance from the relevant regulatory authority.

Highlights of 2012

30

Representative Global Private Equity Partners

Doug Warner

New York

+1 212 310 8751

Kyle Krpata

Silicon Valley

+1 650 802 3093

Marco Compagnoni

London

+44 20 7903 1547

Peter Feist

Hong Kong

+852 3476 9100

peter.feist@weil.com

Michael Weisser

New York

+1 212 310 8249

Kevin Sullivan

Boston

+1 617 772 8348

kevin.sulliv[email protected]

Michael Francies

London

+44 20 7903 1170

Akiko Mikumo

Hong Kong

+852 3476 9088

Michael Aiello

New York

+1 212 310 8552

Scott Parel

Dallas

+1 214 746 7779

David Aknin

Paris

+33 1 4421 9797

Steven Xiang

Beijing/Shanghai

+86 10 6535 5288

Anthony Wang

Shanghai

+86 21 3217 2342

anthony[email protected]

Michael Lubowit

z

New York

+1 212 310 8566

Gerhard Schmidt

Munich

+49 89 24243 101

United States

Europe

Asia

31

About Weil

©2013. All rights reserved. Quotation with attribution is permitted. This publication provides general information and should not be used or taken as legal advice for

specific situations which depend on the evaluation of precise factual circumstances. The views expressed in these articles reflect those of the authors and not

necessarily the views of Weil, Gotshal & Manges LLP. If you would like to add a colleague to our mailing list or if you need to change or remove your name from our

mailing list, please email [email protected].

Weil provides clients with one-stop, global service for sophisticated transactional legal advice.

With more than 400 Private Equity and M&A lawyers worldwide, Weil represents buyers and sellers in the full range

of corporate transactions, including public and private deals, friendly and hostile takeovers, leveraged buyouts,

joint ventures, strategic alliances, spin-offs, venture and growth capital investments, proxy contests, tender offers,

distressed M&A, and public-to-private transactions.

“Weil is world-class –

they have great resources across practice areas.”

— Chambers Global 2012

Weil’s Private Equity and M&A practices are further bolstered by top-ranked, dedicated practice specialists in

Restructuring, Sponsor Finance, Tax, Executive Compensation, Antitrust, Corporate Finance, Governance,

Regulatory, and Technology/Intellectual Property.

“A more holistic view of the attorneys’ transactions shows

a deep client pool and a range in deal types – separating Weil from its

rivals and showing the breadth of its private equity practice.”

— Law360 “Private Equity Group of the Year” January 2013

Weil has a diverse array of deal execution clients, including some of the world’s leading corporations and financial

institutions, and more than 200 sponsor clients that range from some of the most prestigious private equity funds,

hedge funds, sovereign wealth funds, and pension funds to smaller, middle-market funds. With this broad client base,

Weil attorneys have deep exposure to the market and advise on some of the largest, most high-profile, and complex

deals each year.

In 2012, Weil was ranked #1 by Bloomberg for Global Private Equity based on the value of deals announced, with

more than $67 billion in total deal value and 16% of the market. This included more than 15 deals valued at $1 billion

or greater.

“There is a lot of choice out there

but we continue to use Weil because the advice remains relevant.

The lawyers are constantly investing in their industry knowledge.”

— Chambers USA 2011

Weil’s world-renowned M&A practice was ranked #4 by Bloomberg in 2012 for Global Announced Deals, with

approximately $184 billion in total deal value.

Weil, Gotshal & Manges LLP

weil.com

BEIJING

BOSTON

BUDAPEST

DALLAS

DUBAI

FRANKFURT

HONG KONG

HOUSTON

LONDON

MIAMI

MUNICH

NEW YORK

PARIS

PRAGUE

PRINCETON

PROVIDENCE

SHANGHAI

SILICON VALLEY

WARSAW

WASHINGTON, DC

WILMINGTON